Live · CECadence

By Compounding Energy

Live now

GB. SaaS at cadence.compoundingenergy.com, plus on-prem and air-gapped.

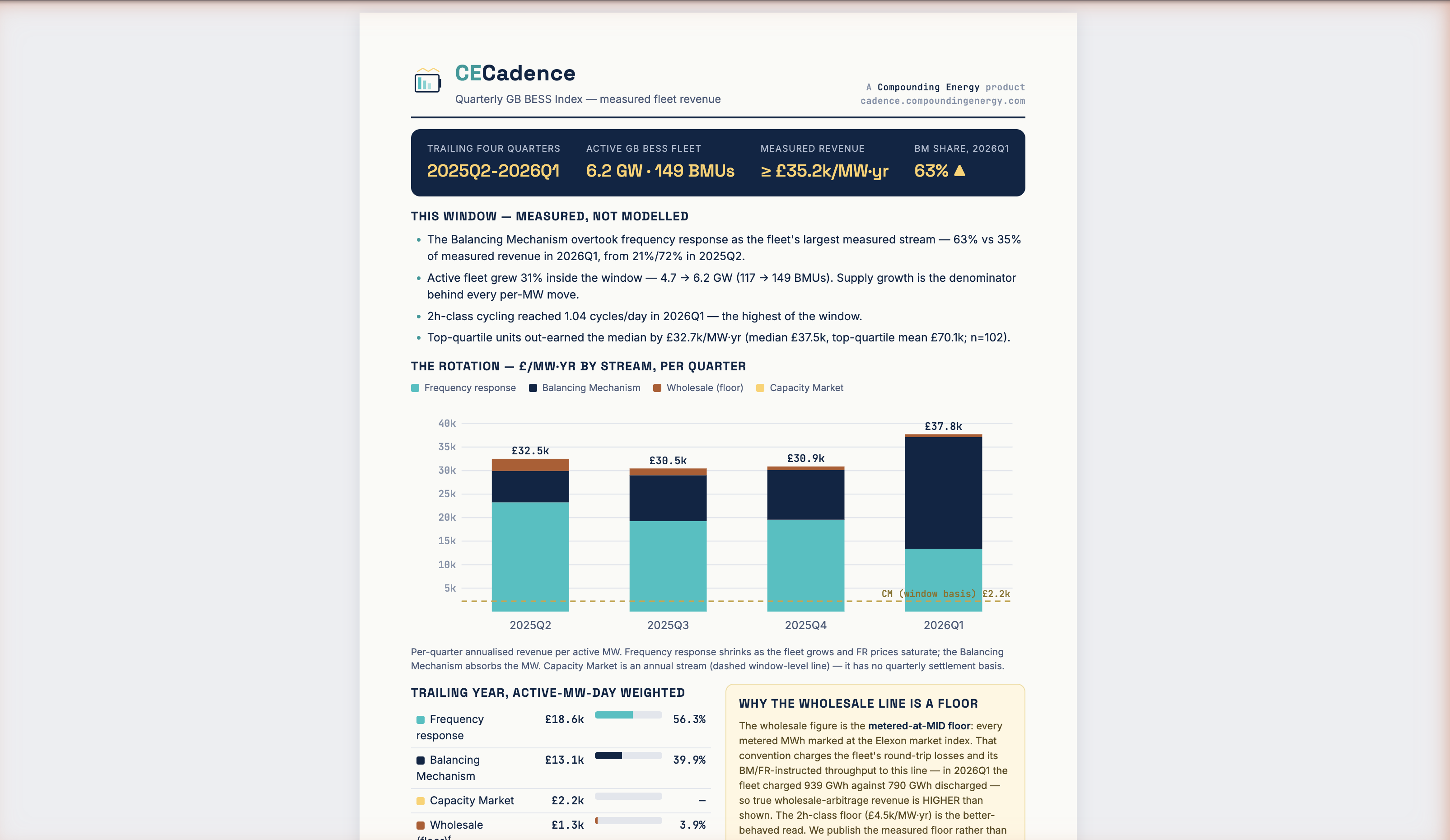

GB battery revenue, forecast at the cannibalisation equilibrium — not the price-taker fantasy.

As more storage is built, batteries compete away the very price spreads they earn from. A naive "price-taker" forecast — which assumes prices are unaffected by the fleet — overstates 2030 BESS revenue by 100–300%+. CECadence solves prices, fleet build-out and dispatch jointly to convergence, and reports the bias — naive minus equilibrium — as a headline number, because that bias is what decides a project's DSCR.